Join the network

Join the network

Blog

Are autocratic states doomed to weak fiscal capacity?

How best to increase and mobilize revenue is a key issue that confronts contemporary developing economies, but the same problems were faced —and solved— by today’s developed economies. In my latest WIDER Working Paper, I turn to history to study how strong fiscal states were built during the last two centuries.

An overlooked insight from the historical data is that fiscal capacity is not exclusively the preserve of democracies, but also of non-democratic states. Understanding the politics of taxation in autocracies is useful to explain the long-term development of fiscal power.

The main take away is this: where legislatures have exercised oversight over governments —for example, by investigating and questioning officials— autocracies have built stronger tax states (compared to autocracies with no or little oversight) by introducing income taxes earlier and collecting more revenue from those taxes.

The problem with the traditional view

State capacity is too often explained as the outcome of either the exigencies of war, or new demands on the state arising from participatory democracy. These explanations ignore state-building efforts that take place in autocratic states in peace time. In fact, key investments in fiscal capacity —such as the income tax— were often made by non-democratic states in the absence of war. For instance, when Britain introduced the first modern income tax in 1842, only 13% of the population had the right to vote. This means there is at least one other, often unconsidered, pathway to improved fiscal capacity.

Building fiscal capacity in autocracy

The number one priority for an autocrat is survival. This requires that the social elite —such as large landowners, wealthy aristocrats, or military leaders— continue to support the regime. The introduction of new fiscal tools (e.g. new taxes) can sometimes threaten this elite since the state might use these tools to expropriate their resources. In order to keep the support of the elite, a ruler needs to promise that new taxes will not be used against them. The credibility of this promise relies on the ability of elites to observe government actions.

When legislatures monitor the government, elites can detect and punish bad behaviour from autocratic rulers. In autocracies with legislatures capable of exercising oversight, new fiscal capacity is therefore unlikely to lead to regime change supported by the social elite. Building fiscal capacity without elite oversight is otherwise dangerous for the autocrat, who risks losing power if the elite perceives the expansion of fiscal power to be a threat.

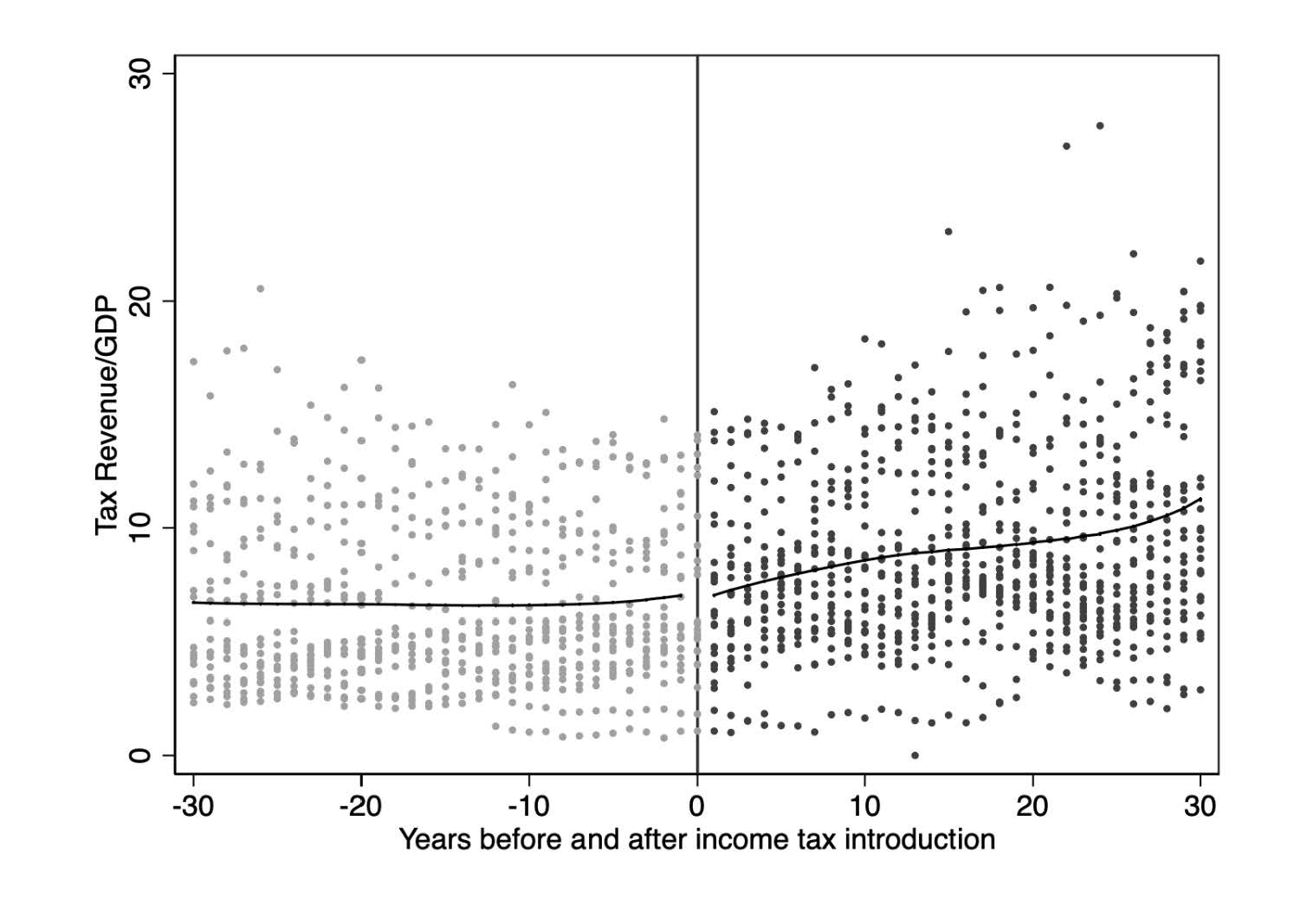

In order to explore this idea, I study the historical introduction and expansion of the income tax. This tax is one of the most significant tax reforms of the last two centuries. Unprecedented in their revenue capacity, income taxes transformed government revenue collection, increasing it from around 5-10% of GDP to closer to 20%.

Figure 1: Tax revenue/GDP before and after the introduction of an income tax

The empirical analysis reveals that autocracies with legislative oversight were indeed more likely to introduce a personal income tax. Moreover —using a new dataset on historical tax revenues— autocracies with legislative oversight were able to collect more revenue from income taxes than those without legislative oversight.

A closer look at the mechanism

While global historical patterns are suggestive, they are unable to tell us about the mechanism at play. To probe the plausibility of the argument, I looked more closely into a historical case of tax capacity building in a non-democratic state: Sweden.

When Sweden adopted the income tax in 1902, it was undemocratic —more than 80% of the adult population lacked voting rights— and there were income and property requirements restricting political participation. But, Sweden did have extensive institutional oversight (for instance, through the Office of the Parliamentary Ombudsman, the legislature exercised oversight over the executive branch).

To finance increased defence spending, as well as major infrastructure projects, new sources of revenue were needed. The income tax was seen as an attractive tool with great revenue potential since it was less volatile and less dependent on international circumstances than tariffs. However, concerns were raised about the privacy of taxpayers.

The information on private citizens which would become available to government bureaucrats made many high-income earners anxious, and efforts were made to alleviate these concerns. Revealing private information was made illegal and tax returns were made confidential.

Elite concerns were overcome in two ways. First, the tax rate was modest and weak on progressivity, and since the elite had many different sources of income, the tax was not a major threat economically.

Second, it was implemented with constitutional checks to protect elites from government overreach. The new income tax was classified as an ‘extraordinary’ tax, and thus under firmer parliamentary control. In practice, this meant taxes could be changed by the legislature without the king being able to veto them. Thus, the reform transferred revenue power from the executive to the legislature. Moreover, the tax did not affect the suffrage (at the time the right to vote was linked to tax payments), which protected the elite against potential redistributive demands from lower classes.

Implications for the contemporary debate

The rise of the fiscal state cannot be explained by democracy and war alone. Many important tax reforms were made by autocracies. There are important institutional differences between autocratic states, differences that matter when explaining tax policy.

These conclusions have two main implications for the contemporary debate. First, strong states can be built even in the absence of violent conflict. That the European path to development was characterized by major wars does not imply that state-building cannot occur in the absence of conflict. Second, even autocracies, viewed by many as political systems inimical to state building, are capable of major fiscal reforms. However, autocracies are not all the same, and how power is organized within these states matters for their ability to invest in fiscal capacity.

My paper highlights an important aspect of capacity building —the ability to trust the government to use fiscal powers in the interest of its constituency. In autocratic states, this means the ability of a small elite to trust the ruler. In a democratic setting, the electorate has institutionalized mechanisms for replacing the government if trust is misplaced. Key in both settings, however, is how institutional solutions such as legislative oversight and executive transparency can build this trust.

Per F. Andersson is a Postdoc at University of Copenhagen and Stockholm University. He holds a PhD in political science from Lund University and studies the politics of tax reform and the relationship between state capacity and regime change.

The views expressed in this piece are those of the author(s), and do not necessarily reflect the views of the Institute or the United Nations University, nor the programme/project donors.