Join the network

Join the network

Research Brief

Revenue losses from tax-motivated mispricing in South Africa

New research provides the first direct evidence of tax-motivated transfer mispricing in a developing country. Using highly detailed firm-level customs data from the tax authority, the analysis calculates the difference between legitimate estimates of market prices (known as the arm’s-length price) to the prices firms actually charge themselves. In the analysis, systematic overpricing of imports is interpreted as strong evidence of tax-motivated transfer mispricing.

The greater the difference in tax rates between jurisdictions, the more firms tend to engage in tax-motivated transfer mispricing

Firms over-charge themselves for imported goods by up to 31% when imports are purchased from an affiliate in a lower tax rate jurisdiction. The analysis does not estimate transfer mispricing for service imports

The average rate of goods mispricing is estimated at 8.59% per import so that a value of nearly 2% of the total tax receipts from multinationals is not collected by the tax authority every year

It may be possible to reduce this revenue leak, worth millions of rand annually, through a digital tax enforcement scheme

What is tax-motivated transfer mispricing?

The current legislation on transfer mispricing in South Africa requires firms to use the arm’s-length price when transacting internally, defined as the price they would pay for a similar good from an external party. When a firm shifts profits from an affiliate in a country with a higher tax rate to an affiliate in a country with a lower tax rate, by overcharging itself for internal transactions, it is known as tax-motivated transfer mispricing. The practice reduces the firms overall tax bill by artificially (and illegally in South Africa) reducing its recorded income.

In a standard analysis, the study finds that firms overprice imports of goods from their own subsidiaries by an average of 31%. When this figure is adjusted to account for all other possible explanations of mispricing (fixed effects), it is reduced to 8.59%. The study therefore concludes that multinational firms in South Africa engage in tax-motivated transfer mispricing of internally transacted goods by at least 8.59%.

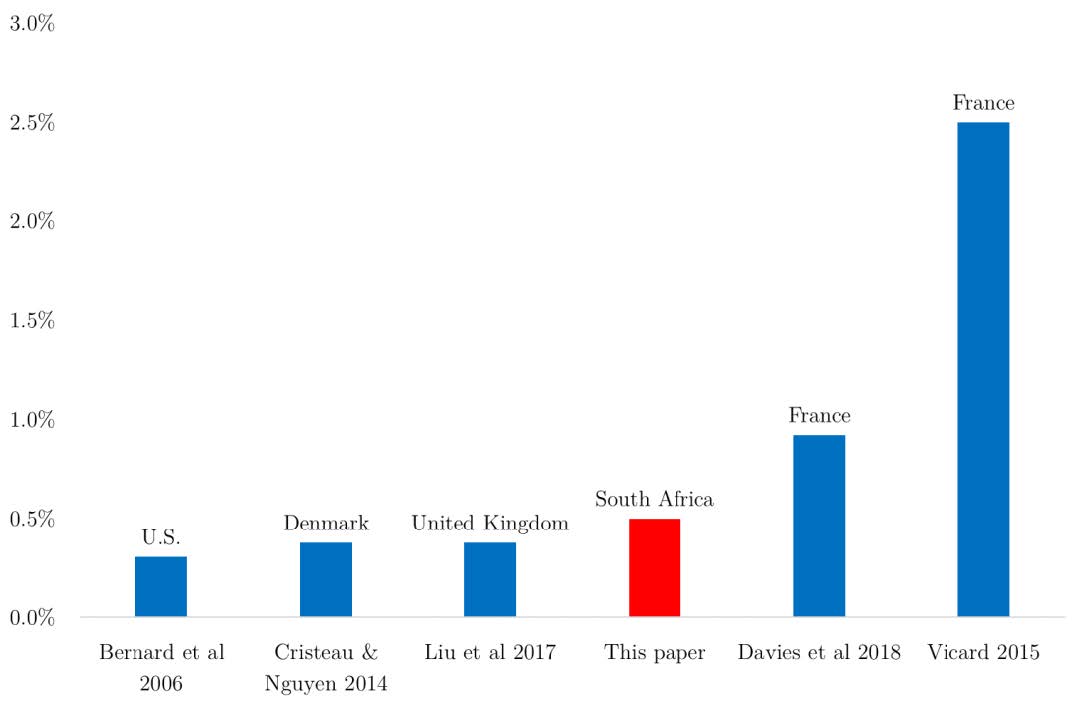

Source: Author’s own literature review (see online appendix).

While the proportionate loss to South Africa, resulting from transfer mispricing of goods, is small, at 0.1% of total tax revenue, the total lost is still several millions of US dollars per year. For example, a 0.1% loss in fiscal year 2012 is equivalent to approximately US$73 million or ZAR1 billion.

The study also estimates that for every percentage point increase in the tax differential between South Africa and lower tax rate jurisdictions, firms increased the price of their internal cross-border transactions, relative to the arm’s-length price, by 2.5%.

The impact of policy reforms

The period of analysis includes a 2012 amendment to South Africa’s legislation on tax-motivated transfer mispricing in accordance with OECD recommendations under the international Base Erosion and Profit Shifting (BEPS) initiative. The research, therefore, is able to track firms’ overall response to a targeted policy measure.

Past research on transfer mispricing has found that a multinational firm’s willingness to engage in illegal transfer mispricing is highly dependent on the difference between its perceived risk of being caught versus its potential gain. More specifically, a willingness to use transfer mispricing should depend on both the likelihood of audits and corresponding penalties from the tax authority — or the risk of being penalized — and the tax differential between the countries the multinational is operating in — or the size of the potential financial gain.

The study finds that the South African legislative amendment of 1 April 2012 on transfer mispricing dramatically, but only temporarily, reduced the rate of transfer mispricing. The estimated price deviation per import fell from over 70% before the reform to under 40% in 2014 after the reform. This is interpreted as firms responding to the reform by expecting greater enforcement from tax authorities. When greater enforcement did not materialize, they resumed their prior behavior, with the estimated price deviation rising to pre-reform levels by 2015.

If this analysis is correct, a credible threat of increased enforcement would have the effect of decreasing tax-motivated transfer mispricing and increasing South Africa’s fiscal revenue.

Policy options

The OECD and the IMF both promote the use of digital tax enforcement to plug revenue leaks. One example would be the establishment of an automatic flagging system at the tax authority as a cost-effective means of increasing the expectation of greater enforcement by the tax authority. For such a system, tax authorities can use their own customs data and a model like the one used for the study to flag firms engaging in transfer mispricing for further audits.

It took two weeks to set up the data in South Africa such that it could automatically flag companies that systematically deviate from the estimated arm’s-length pricing. The costs of doing this are in the thousands of dollars while the potential tax gain is in the tens of millions of dollars. For 2012, the tax loss to South Africa from transfer mispricing was estimated at US$70 million or ZAR1 billion.

While tax-motivated transfer mispricing of goods is a small leak in the state’s revenue collection abilities in relative terms, it is not insubstantial in absolute terms

Increasing the flagging and auditing capacity of the tax authority can boost South African revenue by tens of millions of dollars every year

Continued collaboration with international experts may reveal other practical opportunities to improve the tax enforcement and revenue collection capability of tax authorities

Other emerging economies can also benefit from South Africa’s innovative approach to data and partnership management

As the study did not include multinational firms’ use of transfer mispricing for service and intellectual property rights transactions, the total real revenue loss due to transfer mispricing may be higher. Still, this recommendation, which would only impact mispricing of goods, can still plug a substantial leak in South Africa’s revenue collection.