Join the network

Join the network

Blog

New global estimates on profits in tax havens suggest the tax loss continues to rise

The world has been trying to curb profit shifting to tax havens for a decade, but consistent time series evaluating the impact of these reforms have been largely absent. This column uses a new time series of global profit shifting covering the 1975–19 period to estimate that the fraction of multinational profits (made outside of the headquarter country) shifted to tax havens increased from less than 2% in the 1970s to 37% in 2019, resulting in a tax loss of roughly EUR 250 billion.

In June 2012, world leaders at the G20 meeting in Los Cabos attested to the need to curb the corporate practice of using tax havens. The OECD was put in charge of developing a plan that ended up consisting of 15 tangible actions that should significantly limit abusive corporate tax practices. Three years later, the G20 adopted the plan officially and implementation began across the world in 2016 (Djankov 2021).

In the immediate aftermath of this landmark agreement, leaks of questionable corporate tax practices flooded the ether (the Panama Papers, Paradise Papers and many more). These bolstered public outrage and led to further political action across the world. In the US, the Trump administration passed the Tax Cuts and Jobs Act in late 2017 that almost halved the corporate tax rate in the US and cracked down on profits located in tax havens, both actions intent on lowering the incentive to shift profits to tax havens. Meanwhile Margrethe Vestager —named “the tax lady” by Trump— started going after EU member states granting preferential tax deals to multinationals. Finally, lowering profit shifting to tax havens became an explicit part of the Sustainable Development Goals (SDGs) with SDG 16.4.1.

So, did all of these plans work? Was profit shifting to tax havens curbed by these global efforts? In a new paper (Wier and Zucman 2022), we investigate this and find that it was not. The increase in artificial profit shifting to tax havens by corporations have been relentless since the 1980s until today.

Quantitative estimates of global profit shifting

A body of evidence suggests that multinational companies shift profits to tax havens (e.g. Bolwijn et al. 2018, Clausing 2016, Crivelli et al. 2015, Tørsløv et al. 2022). Until now, however, we have not had a good sense of the dynamic of global profit shifting. Have corporations reduced the amounts they book in tax havens since 2015, or have they found ways to eschew the new regulations? A number of studies provide estimates of global profit shifting, but they typically do so for just one reference year. Moreover, because these studies rely on different raw sources and methodologies, their estimates are not directly comparable, making it hard to construct consistent time series by piecing different data points together.

This limits our ability to study the dynamics of profit shifting and to learn about the effects of the various policies implemented to curb it. This paper attempts to overcome this limitation by creating global profit shifting time series constructed following a common methodology. Our series allow us to characterize changes in the size of global corporate profits, the fraction of these profits booked in relatively low-tax places, and the cost of this shifting for governments of each country.

Our starting point is the estimates from Tørsløv et al. (2022), which are for 2015. Building on the same sources and applying the same methodology, we first extend these estimates to cover the years 2015 to 2019, a period that includes the base erosion and profit shifting (BEPS) process and the US tax reform of 2017. We then construct pre-2015 series back to 1975, which allows us to capture the decades of financial and trade liberalisation that saw a dramatic rise in multinational profits. Due to the lack of some of the input data required to implement the full methodology of Tørsløv et al. (2022), these pre-2015 series are based on additional assumptions and have some margin of error. However, the main quantitative patterns that emerge from these series are likely to be reliable.

Our main findings

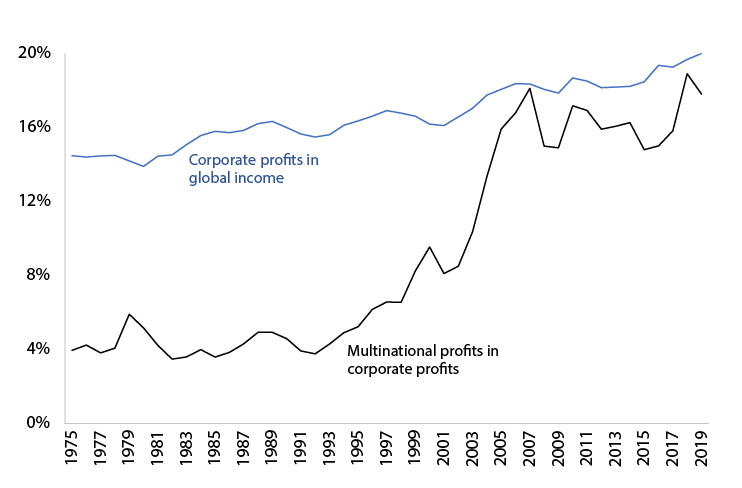

- Global corporate profits grew much faster than global income between 1975 and 2019. The share of profits in global income increased by a third over this period, from about 15% to close to 20%. This increase is due both to the rise of the share of global output originating from corporations (as opposed to, for example, non-corporate businesses) and the rise of the capital share of corporate output. The fast growth of corporate profits means that if the effective global corporate income tax rate had stayed constant, global corporate tax revenues (as a fraction of global income) should have increased by about one third since 1975. In reality, corporate tax collection has stagnated relative to global income – that is, the global effective corporate income tax rate has declined by about a third.

- There has been a large rise in multinational profits, defined as profits booked by corporations in a country other than their headquarters. The share of multinational profits in global profits has more than quadrupled since 1975, from about 4% to about 18%. This evolution reflects the rise of multinational firms, a well-known development but for which a global quantification was lacking so far. The rise has been particularly pronounced since the beginning of the 21st century. This evolution may explain why the issue of how to tax multinational firms has become more salient in the first two decades of the 21st century. When foreign profits accounted for only about 5% of global profits (as was the case from the 1970s through to the late 1990s), the tax revenues implications of properly taxing these profits were relatively small. With the rise of multinational profits, the revenue implications are significantly larger.

Figure 1: Corporate profits (% of income) and multinational profits (% of all profits)

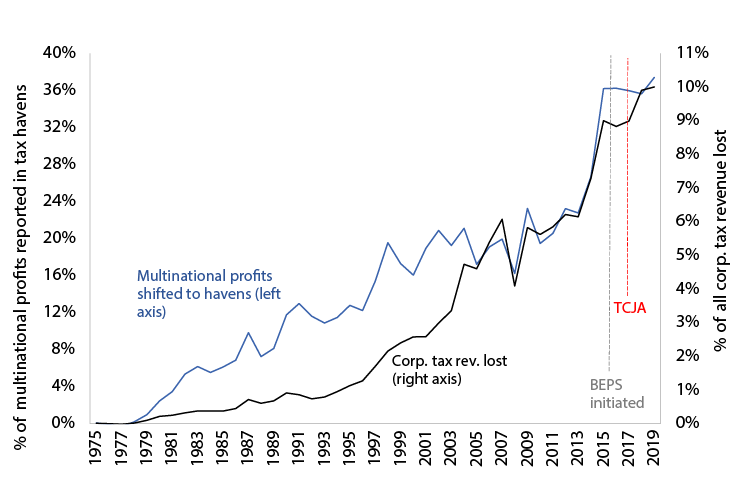

- There has been an upsurge in the fraction of multinational profits shifted to tax havens. By our estimates, this fraction has increased from less than 2% in the 1970s to 37% in 2019. Because multinational profits themselves have been rising much faster than global profits, the fraction of global profits (multinational and non-multinational) shifted to tax havens has risen from 0.1% to about 7%. Consistent with these findings, we estimate that the corporate tax lost from global profit shifting has increased from less than 0.1% of corporate tax revenues in the 1970s to 10% in 2019. The tax loss is slightly higher than the fraction of profits shifted to tax havens globally because the marginal rate on shifted profits is higher than the average rate.

Figure 2: Multinational profits in tax havens and corporate tax lost

- In 2019 – four years into the implementation of the BEPS process and two years after the Tax Cuts and Jobs Act – there was no discernible decline in global profit shifting or in profit shifting by US multinationals (which, according to our estimates, account for about half of global profit shifting) relative to 2015. Of course, it is possible that absent BEPS and the Tax Cuts and Jobs Act, profit shifting would have kept increasing; we do not argue these initiatives had no effect. However, their effect seems, so far, to have been insufficient to lead to a reduction in the global amount of profit shifted offshore. This finding suggests that there remains scope for additional policy initiatives to significantly reduce global profit shifting.

Authors’ note: The views in this column are the authors’ and not necessarily those of the Danish Ministry of Finance or UNU-WIDER. All of our research is available in the public database missingprofits.world. Here you can see the individual tax losses (or gains) of each country using our interactive map. You can also find the methodology description that was recently published in the Review of Economic Studies. We will continue to update our results as new data become available.

References

Bolwijn, R, B Casella and D Rigo (2018), An FDI-Driven Approach to Measuring the Scale and Economic Impact of BEPS, Transnational Corporations 25(2): 107–43.

Clausing, K A (2016), The Effect of Profit Shifting on the Corporate Tax Base in the United States and Beyond, National Tax Journal 69(4): 905–34.

Crivelli, E, R de Mooij and M Keen (2015), Base Erosion, Profit Shifting and Developing Countries, IMF Working Paper 2015/118.

Djankov, S (2021), Simpler approaches to a global tax plan, VoxEU.org, 8 October.

Tørsløv, T, L Wier, and G Zucman (2022), The Missing Profits of Nations, The Review of Economic Studies, rdac049 (see also the Vox column here).

Wier, L and Zucman, G (2022), Global profit shifting, 1975–2019, UNU-WIDER Working Paper No. wp-2022-121.