Join the network

Join the network

Blog

35 years of knowledge for change

Changing IMF orthodoxy (1985-95)

UNU-WIDER was among the first to challenge IMF orthodoxy on macroeconomic stabilization. The 1985-87 project ‘Stabilization and adjustment policies and programmes’ put out a set of work that stands today as one of the first critical and credible collections calling for reconsideration of IMF structural adjustment programmes. This seminal research continues to impact development discourse, with calls for change continuing to reverberate today.

What used to be heresy is now endorsed as orthodox.

— John Maynard Keynes, 1944

The International Monetary Fund (IMF) plays a critical role in the global system as the world’s lender of last resort. That means it provides balance-of-payments support to governments during crises – when countries are all out of options – with a critical mandate to stabilize the global system and prevent crisis transmission and economic collapse. All too often, though, the IMF faces criticism for using its leverage to pressure poor and crisis-stricken countries into adopting ‘misguided' policy packages that ultimately become the de facto stabilization, recovery, and development policy of the nations in its debt.

An IMF crisis of relevancy

In 2007, there was a brief moment of global economic euphoria – poverty rates were declining faster than they ever had, major development goals were on track, economies were booming, and the outstanding debt owed to the IMF – a crucial inverse indicator of global economic health – hit an all-time low. Commentators wondered out loud if the IMF had lost its relevance. For the not insubstantial numbers of people that see the IMF as the instrument of a failed one-size-fits all economic policy, venomously coined the ‘Washington Consensus’ by analysts, activists, and political leaders, some of whom view the institute as a collaborator in U.S. economic imperialism, the declining power of the IMF was cause to celebrate.

On 1 March, 2007 The New York Times published these words about the IMF:

'The international lender's worldwide portfolio has shriveled to $11.8 billion from a peak of $81 billion in 2004, and a single country, Turkey, now accounts for about 75 percent. As its lending wanes, so does the fund's ability to influence government policies. The IMF and its sister institution, the World Bank, have used aid to promote free trade, unfettered investment flows and limited government.'

The left-leaning leaders of several Latin American countries during the early 2000s felt that by freeing themselves of IMF debt and IMF influence, they would finally be free to pursue a path to prosperity. Argentinian President, Nestor Kirchner, told a gathering of world leaders in April 2005, after seeing a two-year economic growth rate of 9%, 'This is life after the IMF, and it’s a good life.' Venezuelan President, Hugo Chavez, speaking to G-15 leaders at its 13th Annual Summit, said 'We don't accept the kind of development the World Bank and International Monetary Fund want to push on us.'

Putting their money where their mouths were, Latin American leaders collaborated to rapidly pay down their outstanding IMF debt. One week after Brazil made good on its debt with a single 15.5 billion USD lump-sum payment in December of 2005, Argentina followed suit with nearly 10 billion USD put up, a sum made possible by help from Venezuela, who had pledged to purchase up to 3 billion USD in Argentine bonds to help the country kick out its IMF creditors. Countries around the world were following suit, shrinking the IMF account ledger to a 2007-low and ushering in a round of questions about the IMF’s role in the world.

IMF still standing

For all the bluster of the 2000s and the growing consensus that the IMF was in need of further reforms, no country caught in the blast perimeter of the financial explosion that was the Wall Street crisis of 2007-08, could deny the instrumental role that IMF lending plays in maintaining global stability. By 2010 the IMF ledger was back up to 60.5 billion from the 2007 low of 9.8 billion. The eurozone crisis soon followed and, as is often the case, rich country problems quickly became poor country ones. By 2012, the IMF balance hit a new all-time peak of 95.8 billion and claims of IMF irrelevancy in the new century were put to rest.

For a time thereafter, the IMF ledger improved. But once again, today, as the world grapples with the fall-out from COVID-19, the necessary role of the fund is demonstrable. The IMF ledger hit a new all-time record high just last month – of 97.1 billion – and this is seen as much too small a sum for what is needed – with both UNCTAD and the IMF estimating a USD 2.5 trillion need.

Criticism of the IMF is a mainstay of the global system

Both the need for a global lender of last resort, of which there is only the IMF, and a need to reform this lender are often argued equally. Criticism of different aspects of the IMF – including who leads it and where it is located (Washington D.C.) – has become as much a mainstay of the global system as the IMF itself.

For example, this year we have already heard calls to reform the way that the IMF issues its currency, Special Drawing Rights (SDRs), and to expand its stance on capital account regulations. Following a sustained campaign from emerging markets and other critics, the IMF made major reforms in how it allocates votes among member states in 2010 and in 2016 – giving middle-income countries a greater say. In 2009, the IMF implemented reforms to conditionality, one of the most criticized of its modus operandi. And, in 2001, responding to 25 years of global pressure, most visibly spearheaded by the Jubilee 2000 movement, the IMF discharged a swath of debt owed by 23 of the highly-indebted poor countries (HIPC).

The origins of the IMF’s reputational problem date back to the 1970s, when ‘macroeconomic shocks in avalanche proportions hit developing countries’. When the IMF arrived to bail-out struggling and suddenly highly-indebted countries in the Global South, they quickly exchanged emergency financing for agreements from national policymakers to embark on the stabilization packages that would later come to be known, quite infamously, as Structural Adjustment Programmes (SAPs).

The countries which encountered crises between 1974-82, failed to recover from the initial shocks – in many cases for more than a decade. For those countries, those decades have come to be known as the Lost Decades – shorthand for the lost decades of global development, a reference to the 1970s and 1980s second and third UN Decades of Development, during which stagnation was more prevalent than progress. The infamy of early SAPs is largely credit to what is broadly seen as their abject failure. But it is also credit to a rising tide of critical voices pointing out this failure, among which sits a core set of influential UNU-WIDER work.

IMF orthodoxy under fire

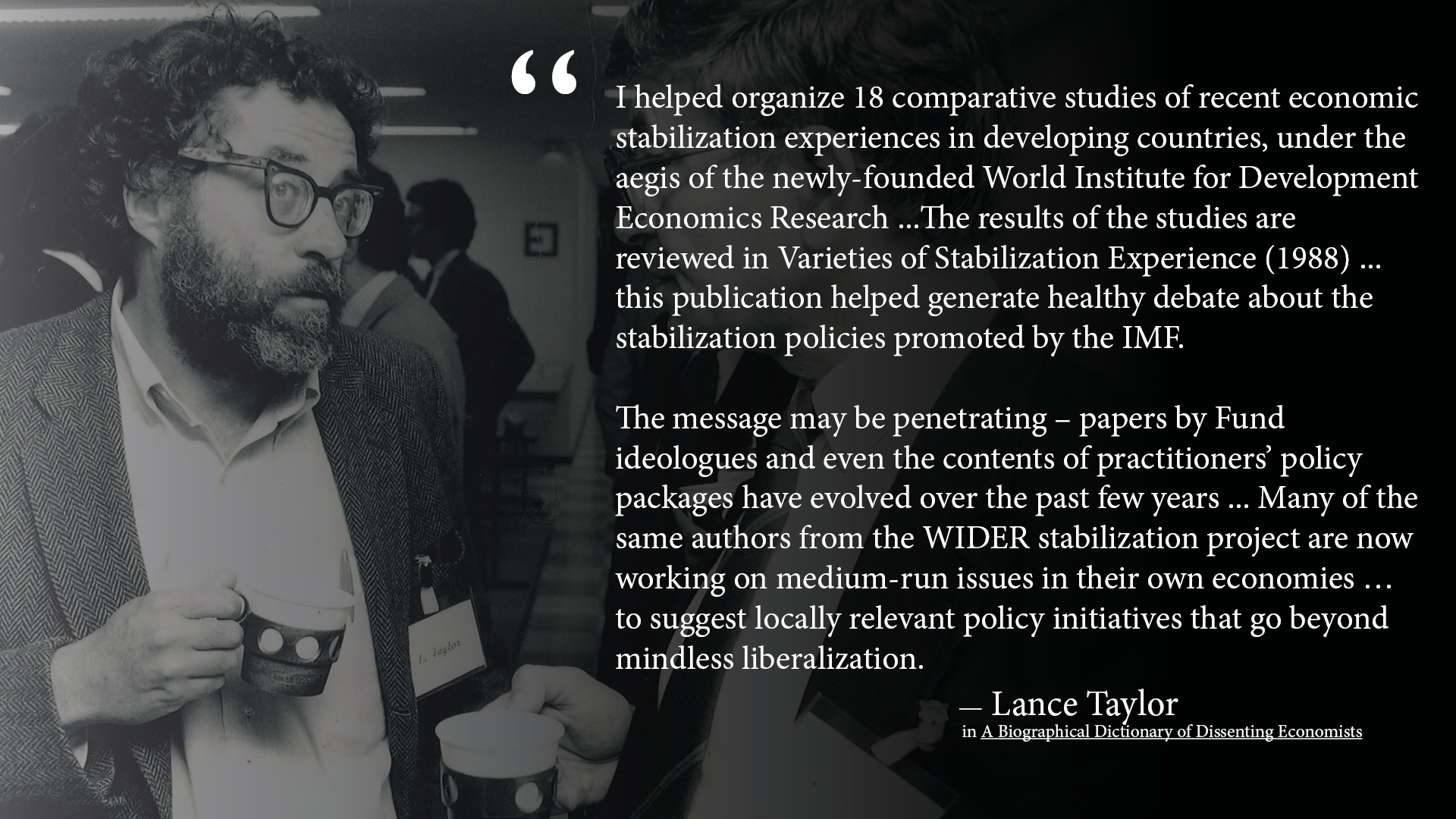

The UNU-WIDER project ‘Stabilization and adjustment policies and programmes’ undertaken from 1985-87 with leadership from Lance Taylor and Gerry Helleiner, put out a set of work that stands today as one of the first critical and credible collection of voices calling for reconsideration of IMF SAPs. The project carried out 17 country case studies on developing countries that had recent experience with IMF-involved stabilization programmes. Many of these case studies were written by experienced developing country nationals – a hallmark of UNU-WIDER’s work – experts like Benno Ndulu, who have gone on to have distinguished careers in development policy and research.

These country case studies are collected in the UNU-WIDER book A Rocky Road to Reform edited by Lance Taylor and their lessons are synthesized in the UNU-WIDER book Varieties of Stabilization Experience. Both works set in motion the massive body of research that we have today on how best to support developing economies during macroeconomic crises, a body of work that has been instrumental in changing the global system for the better.

As Lance Taylor argues about these early studies, in the introduction to Varieties of Stabilization experience, 'Their principal finding is that past policies could have been designed to better effect, and that programmes of the Fund/Bank [IMF/World Bank] type are optimal for neither stabilization nor growth.'

According to former UNU-WIDER director Lal Jayawardena, the Rocky Road to Reform answers the question: 'The degree to which this standard approach [to macroeconomic stabilization] was relevant or successful [and] whether alternative policy packages could have been devised … at a lower social cost than that incurred by the country packages that were in fact negotiated.'

The project’s central contribution to development discourse goes beyond joining a 25-year long chorus of voices calling for change, and sometimes succeeding, at the IMF. And, it goes beyond making fundamental contributions to the way that the global system and developing countries partner to overcome major macroeconomic disruptions, like the one we are seeing today as a result of COVID-19. The project’s work helped originate the once-heterodox/now-mainstream idea that policy solutions for developing economies cannot be one-size-fits-all and that both development research and policy praxis must be diagnostic, and evidence- and -experience-based in its approach.

As Lal Jayawardena prophetically wrote of the project soon after its completion:

'The wealth of country-based experience has clearly established the need for a departure from the earlier perspective of a standard approach [and] highlights the need to formulate these programmes in a manner appropriate to the institutional and structural characteristics of the economy in question.'

The views expressed in this piece are those of the author(s), and do not necessarily reflect the views of the Institute or the United Nations University, nor the programme/project donors.