Join the network

Join the network

Blog

Will Norway’s model of Sovereign Wealth Fund work in Tanzania?

A reality check

Several countries in Africa – including Ghana, Kenya, Mozambique, Tanzania, and Uganda - have recently discovered large oil and gas or other mineral resources. Other African countries such as Angola, Botswana, and Nigeria have been exploiting very large extractive wealth for many years. Natural resource wealth has often turned out to be a ‘curse’ rather than a ‘blessing’ for developing countries. The UNU-WIDER project ’Extractives for development’ aims to find ways in which resource wealth could be managed more successfully in developing countries.

The newer extractive countries are rightly being encouraged to think carefully about how best to utilize the large additional government revenues from extractives (profit-share and taxes) that they now expect. They are being advised in particular to address the inter-generational issues. The establishment of some form of Sovereign Wealth Fund (SWF) is being mooted in almost all cases, and the example of the SWF of Norway is invariably referred to as an illustration of the benefits that such an institution might deliver. But what might this mean in practice and how viable might be any suggestion for, say Tanzania to build its proposed new Natural Resource Governance Fund on the Norwegian model?

Norway - scale, credibility, and legitimacy

In 25 years, the Norwegian SWF has accumulated assets that amount to almost $900 billion. That is equivalent to $178,000 for every one of Norway’s 5 million population (adults and children) or more than $700,000 for a typical family of four. In the years since the fund was established, Norway has typically enjoyed large fiscal surpluses – often around 10% of GDP with oil and gas revenues contributing a significant part of this. Per capita income in Norway is circa $100,000. So if the government is able to invest even 40 per cent of these surpluses into the SWF then this is equivalent to adding another $4,000 a year to each Norwegian’s implicit stake even before factoring in a real (inflation-adjusted) rate of return of more than four per cent per annum. Further, because the fund is so large, it can easily cover large absolute amounts of administrative costs, which still amount to much less than one half of one per cent of the fund’s total assets. Above all, the Norwegian fund enjoys a high level of credibility and legitimacy (in the eyes of the public, the government and the investor community) and has been able to retain this even in those years where it has realized very large portfolio losses (as much as 25% of its total asset value in some years).

Tanzania’s SWF – the Natural Resources Governance Fund

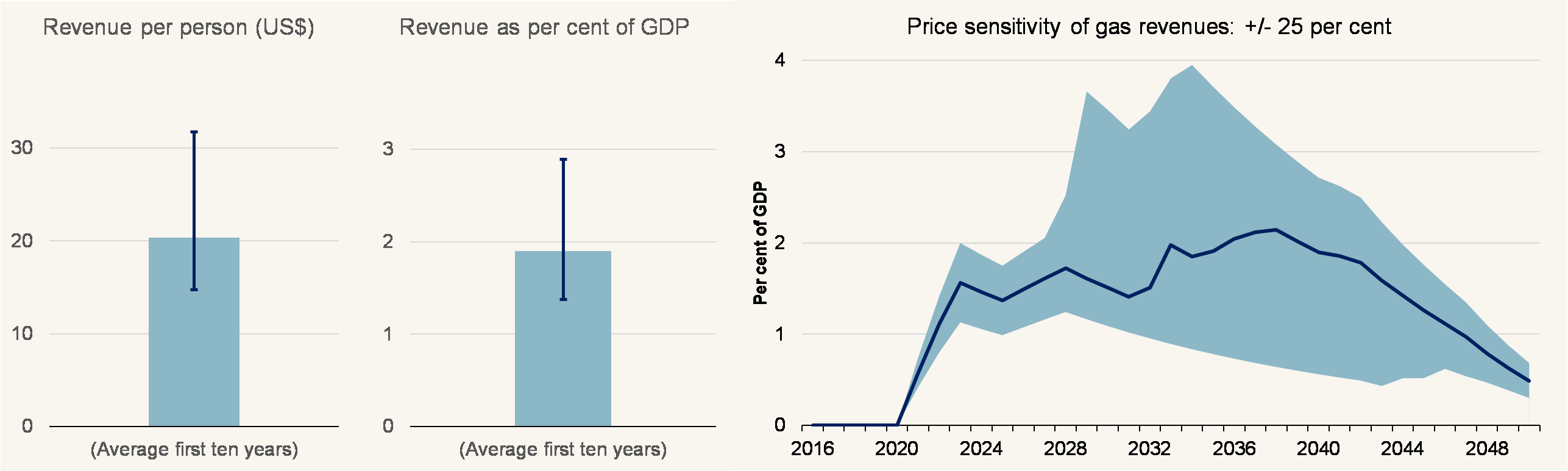

Tanzania has for many years run significant fiscal deficits – typically around 3-5% of GDP. The projected improvements to this situation associated with the huge new gas funds in the Indian Ocean are estimated to be of the order of 1% to 4% of GDP (depending on year and the prevailing world prices for gas/LNG) - see Figure below. In other words, even after factoring in the huge and unprecedented windfall from natural gas, Tanzania’s future budgets seem likely, at best to be in balance or have only a small overall surplus. It seems unlikely that Tanzania could commit to investing more than a small amount to its SWF on an annual and long-term basis.

Tanzania: Projections of government revenues from natural gas

Let us assume nonetheless that the government can still commit an average of, say 0.5% of GDP per annum to the new Natural Resources Governance Fund. Given Tanzania’s per capita income of circa $1,000 and a population of 50 million this will build capital at the rate of $5 per capita and $250 million per annum. So it will take a very long time to build up a fund of any size. For example, after some ten years – assuming a steady gas price and no withdrawals – the fund would grow to a total of $2.5 billion plus net interest on the accumulating capital balance: circa $50 per capita. This sum would be broadly equal to the amount that Tanzania has been spending annually in recent years on its development budget (5% of GDP); but equivalent to only one third of its typical annual recurrent expenditures (circa 15% of GDP).

This is not a trivial sum. The Tanzanian authorities, if they could pull it off through two or three election cycles could be commended for making the considerable sacrifices of short-term budget expenditures for the benefit of later generations. But let us be clear what the success will imply. First it will mean that, for each and every one of the ten years of our example, budget officers will need to win the difficult battle of withholding from line ministries the not inconsiderable sum of 0.5% of GDP. Second, it means that stringent rules have to be set up and enforced to protect the growing fund (e.g. at least 0.5%, 1,0%, 1,5% etc. of GDP in successive years) from those same line ministries all of whom will have compelling spending requirements. This sustained mutual self-restraint will represent a major political-economy challenge. Third, the application of a high discount rate – justified by Tanzania’s severe poverty situation – would likely show that the accumulated capital in the SWF after ten years of $2.5 billion plus the accumulated returns might in NPV terms be lower than the accumulated sums that have been withheld from current spending. This outcome is all the more likely because the small scale of the fund would probably subject it to far higher administrative costs in percentage terms (than in Norway) even if management and other inefficiencies could be avoided. Finally, and most importantly, is it likely that the credibility of a fund that aspires to achieve a sustained transfer of wealth from the present to some date far in the future can be established?

There is more than one way to manage sovereign wealth

This is not an argument against the prudent step of setting aside extractive windfalls in an attempt to preserve some of that wealth for the future. But it is an argument against the assumption that there are pre-existing SWF models that have built credibility and so societal legitimacy over many years that can readily generate the same benefits if transplanted into a low-income African context. There are other ways to manage the inter-generational problem and maybe these should also be explored.

For more on the topic of sovereign wealth funds and the management of extractives in general, be sure to bookmark the Extractives for development, as well as the WIDERAngle blog. Follow #ManagingExtractives on 11-12 April for live updates on our Extractive industries and development meeting, where topics including regulation, macroeconomic management, and inclusivity and sustainability will be discussed. An open access book considering these topics in more detail is forthcoming and will be announced on our website.